How to downsize in Sydney after 60

A practical 2026 guide for homeowners who want less stress, more clarity, and a better next chapter

Downsizing in Sydney after 60 sounds simple when people say it quickly.

Sell the family home. Buy something smaller. Free up some cash. Move on.

In real life, it rarely feels that neat.

For many Sydney homeowners, the house is not just an asset. It is decades of memory, a major part of retirement security, and often the single biggest financial decision they will make in the next ten or twenty years. That is why downsizing can feel exciting and heavy at the same time. On one hand, it can unlock flexibility, reduce maintenance, and free up capital. On the other, it can raise difficult questions about timing, location, pension impacts, moving costs, family expectations, and whether the next home will truly suit your lifestyle.

That tension is exactly why many people delay the decision for years.

The good news is that downsizing does not need to be rushed, reactive, or confusing. Done well, it becomes a structured process. You work out what you want life to look like next. You understand your numbers. You test the trade-offs. You build the right support around you. Then you move when the timing and the strategy make sense.

In Sydney, this matters even more because the stakes are high. A long-held home can contain substantial equity. Buying again in NSW usually means transfer duty applies. If you are receiving Age Pension, the treatment of sale proceeds and assets can affect your position. If you want to use the downsizer contribution, there are specific eligibility rules and timing requirements.

This guide is designed to help you think clearly about all of it.

It is not just about “moving smaller.” It is about making a better property decision, a better retirement decision, and often a better lifestyle decision.

Why so many Sydney homeowners downsize after 60

There is usually more than one reason.

For some people, the trigger is practical. The stairs are becoming annoying. The garden is too much work. The house feels too large for one or two people. For others, it is financial. Too much wealth is tied up in a home that does not generate income. They want to free up capital for retirement, travel, family, or simply a bigger margin of safety.

Then there is the emotional side. A lot of people do not want to “downsize” because the word itself can sound like a loss. In reality, the better frame is often this: you are not necessarily downgrading your life, you are resizing it to suit the next stage.

Sydney also creates its own pressure. Many older homeowners bought well before the city’s major property appreciation. That means the gap between what they own and what they might need next can be substantial. A move from a long-held family home to a smaller, better-located property can sometimes release hundreds of thousands of dollars, and in some cases much more. At the same time, Sydney buyers also face meaningful transaction costs, especially transfer duty on the replacement property in NSW.

The most successful downsizers tend to see the move as a whole-of-life decision, not just a real estate transaction.

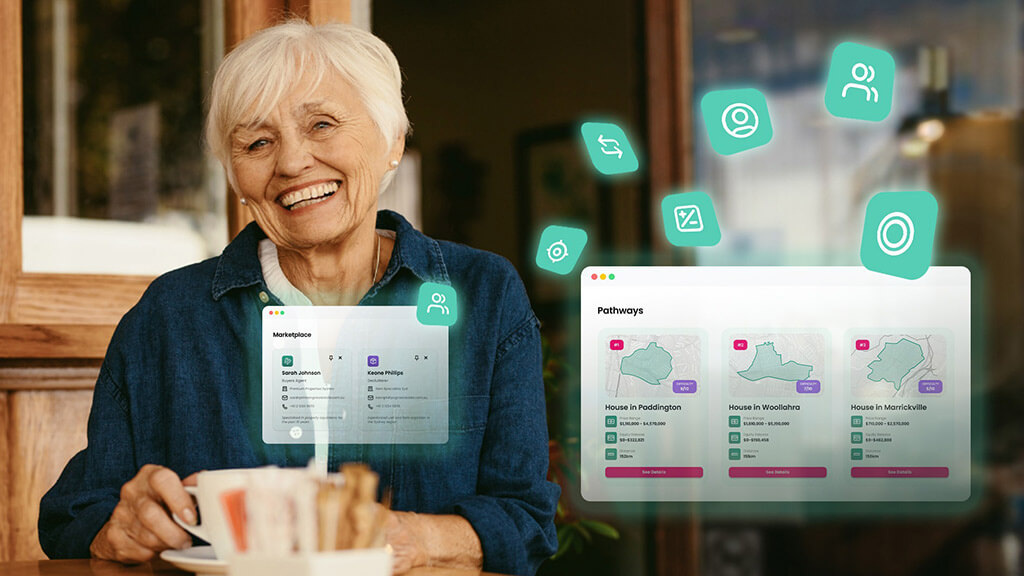

How iDownsize can help before you make any big decisions

This is the stage where most people do one of two things: they either over-research and get stuck, or they start talking to providers too early and feel pressured.

iDownsize works best here as a planning layer.

Instead of jumping straight into sale conversations or finance discussions, you can start by organising your own situation through the features you need. That makes it easier to understand where you are in the journey, what you are trying to achieve, what kind of support you may need, and what questions you want answered first.

For someone still in research mode, that might mean comparing suburb options, exploring estimated home value and equity, or understanding whether sell-first or buy-first is likely to fit their situation better. For someone further along, it might mean using the Provider Network to identify which professionals could help at each stage without rushing into a decision before they are ready.

Step 1: Start with the outcome, not the property

One of the most common downsizing mistakes is starting with listings.

People open property portals, look at apartments or villas, and begin judging options before they have decided what they actually want their next life stage to look like. That usually leads to confusion because the real question is not “What can I buy?” It is “What am I trying to improve?”

For some people, the answer is convenience. They want cafés, transport, medical services, and shops nearby so they can drive less and do more on foot. For others, it is simplicity. Less cleaning, less maintenance, less wasted space. For others, it is financial. They want to release capital, reduce ongoing costs, and build more flexibility into retirement.

Write that down first.

A useful way to think about it is to define your downsizing goals across four areas:

- Lifestyle. How do you want day-to-day life to feel? Easier? More social? Closer to family? More walkable?

- Property. What kind of home would suit the next ten to twenty years? Single level? Lift access? Lower maintenance? Space for guests but not excess?

- Financial outcome. How much equity would you ideally like to release? Are you trying to strengthen retirement income, fund renovations in the next property, travel more, or create a buffer?

- Timing. Are you just exploring? Are you hoping to move within a year? Or are you actively preparing now?

These questions sound basic, but they are foundational. Someone whose main goal is community and convenience will make very different suburb and property choices from someone whose main goal is maximising net cash released.

How iDownsize can help at this stage

This is a strong point to use the platform’s Pathways feature.

A lot of people are not ready to buy or sell yet, but they are ready to organise their thinking. Pathways helps turn a vague idea into a clearer plan by showing practical next steps based on where you are in the downsizing journey.

That can stop the common pattern of either drifting for months or jumping too quickly into provider conversations before you are ready.

Step 2: Understand your real numbers, not just your headline equity

A surprising number of homeowners think they know what downsizing will achieve financially, but are working off a rough, flattering estimate.

They might say, “Our home is worth about $2.4 million and we’ll buy for around $1.6 million, so we should free up roughly $800,000.”

Sometimes that is directionally true. Often it is not.

The reason is that downsizing outcomes are shaped by more than the sale price and the next purchase price. You need to allow for sale costs, legal fees, marketing, possible styling or minor works, moving costs, and the buying side costs that people often underestimate.

Here is a cleaner way to think about it.

Start with the likely sale range of your current home, not the highest optimistic number. Then subtract a realistic allowance for agent fees and sale preparation. Then estimate your buy range, not just a single purchase figure. Then add transfer duty and associated acquisition costs. Only after that do you get closer to the number that matters: what you are likely to retain after the move.

A realistic Sydney scenario

Imagine a couple in their late sixties living in a freestanding home in Sydney’s north-west.

They believe their current home may sell for around $2.1 million. After agent fees, marketing, styling, conveyancing, and some minor presentation work, total sale-side costs might take a noticeable bite out of proceeds. They then purchase a townhouse or apartment for $1.45 million in an area that offers better walkability and easier upkeep. On top of that purchase comes transfer duty and legal costs. By the time everything is done, the amount actually released may look very different from the casual “sale price minus purchase price” estimate they started with.

That difference matters because it affects everything else: retirement planning, super strategy, cash buffer, pension position, and how aggressive or conservative they can be with the next purchase.

How iDownsize can help at this stage

This is where the Downsize Calculator becomes genuinely useful.

Rather than relying on rough guesses, you can use it to start grounding the conversation in your likely numbers. That makes your next decisions smarter and gives you a clearer idea of whether your move is mainly about lifestyle, cash release, or a mix of both.

Step 3: Decide whether you are solving for certainty or convenience

This is the famous sell-first versus buy-first question.

It gets a lot of attention because it is not just a tactical choice. It reveals what kind of risk you are willing to carry.

Selling first generally gives you more certainty. You know what your current property actually sold for. You know the capital available. You reduce the chance of buying your next home based on an optimistic assumption about your sale price. That can be especially valuable in a changing market.

Buying first, on the other hand, can reduce disruption. You may avoid temporary accommodation. You may secure the right property when it appears. The move can feel more seamless. But it usually requires a stronger finance strategy and a higher tolerance for timing risk.

There is no universal right answer. But there is usually a right answer for your situation.

If you are highly risk-averse, want budget certainty, or would feel stressed by holding two properties or bridging a timing gap, selling first often makes sense. If the perfect next property matters more than convenience, or if your circumstances make temporary living especially disruptive, buying first may be worth exploring.

The mistake is treating this as a simple preference question. It is really a risk-structure question.

For a deeper breakdown, read Sell First or Buy First in NSW?.

How iDownsize can help at this stage

This is a natural point for the Provider Network feature.

A reader at this stage often needs a way to pressure-test their thinking. A mortgage broker may help test what buy-first could look like financially. A buyers agent may help assess whether a scarce property type is worth securing first. A real estate agent may help calibrate sale timing and local demand.

The platform can also help you access off-market properties, which may be especially useful if you are trying to secure the right next home before going fully public with your plans.

Step 4: Choose the suburb based on the life you want, not the suburb you know

A lot of downsizers instinctively want to stay close to where they have always lived. Sometimes that is the right choice. Sometimes it is just familiarity masquerading as strategy.

The better question is not “Where have we always been?” It is “Where will our next stage work best?”

In Sydney, suburb choice is not only about price. It is about transport, topography, access to services, social connection, walkability, noise, density, parking, and how the suburb feels on an ordinary Tuesday, not just at an inspection.

For some downsizers, the ideal move is into a nearby apartment or villa that keeps them close to existing networks. For others, the better decision is to shift into a more convenient hub with shops, healthcare, and transport within easy reach. Some want lower-density coastal living. Some want vibrant inner-city access. Some want a quieter village feel with enough amenity to reduce dependence on driving.

This is where many people go wrong: they focus on “property specs” before “location function.”

A beautiful apartment can still be the wrong downsizer move if the street is too steep, parking is awkward, public transport is poor, or the local amenity does not support how you actually want to live.

How iDownsize can help at this stage

This is where the Suburb Navigation feature becomes powerful.

Instead of browsing by vague instinct alone, you can compare suburbs in a way that is more aligned to downsizer decision-making: convenience, services, liveability, and suitability for the next phase of life.

Step 5: Compare properties more clearly and objectively

One of the hardest parts of downsizing is that the “right” property is rarely obvious.

You may be comparing an apartment close to transport, a townhouse with more space, or a villa in a quieter suburb. Each option can look appealing for different reasons, which makes it easy to second-guess yourself or compare them emotionally instead of strategically.

That is why it helps to compare replacement properties using the same criteria each time: price, layout, accessibility, ongoing maintenance, strata or body corporate implications, location convenience, parking, and long-term suitability.

Without a clear comparison method, many downsizers end up focusing too heavily on cosmetic appeal or square metre differences and not enough on how the property will function in everyday life.

How iDownsize can help at this stage

This is exactly where the Property Comparison feature adds value.

It helps you compare different homes more clearly, which is especially useful when several options look good on the surface but only one or two really suit your goals, budget, and lifestyle.

Step 6: Build your downsizing team in the right order

Downsizing often becomes stressful because too many people enter the process at once.

You do not always need the full team on day one. What you usually need is the right person at the right stage.

Early on, you may need clarity more than execution. That might mean using tools, content, and light-touch guidance to understand the likely shape of your move. Once you move into planning, different needs emerge: sale advice, suburb strategy, buying support, financial implications, legal timing, move logistics.

The right mix may include a real estate agent, a buyers agent, a mortgage broker, a financial adviser, legal services, decluttering services, and removalists. But not all at once, and not in a random order.

The smartest downsizers sequence support. They do not outsource their judgment. They use providers to strengthen it.

How iDownsize can help at this stage

This is another point where the Provider Network is helpful.

Rather than trying to source everyone separately, you can explore which type of support may matter next and build the right team progressively as your plan becomes clearer.

Step 7: Prepare your current home for sale without turning it into a second full-time job

This is the stage people often underestimate emotionally.

The practical tasks are obvious enough: decluttering, repairs, presentation, decisions about what stays and what goes. But the emotional weight can be larger than expected, especially when a home contains decades of life.

That is why sale preparation is not just about getting a better price. It is about reducing chaos.

The key is not to ask, “How do we perfectly prepare this home?” It is to ask, “How do we prepare it efficiently enough to support our goal?”

Sometimes that means a basic tidy and sale. Sometimes it means more deliberate presentation because the likely uplift justifies the effort. What matters is that the plan aligns with the broader downsizing outcome rather than becoming an endless project.

How iDownsize can help at this stage

When preparation starts to feel overwhelming, it helps to go back to the features you need and identify what kind of support will reduce the burden most.

That may be a real estate agent, decluttering support, removalists, or another provider who can make the move more manageable.

Step 8: Understand the super and pension angles before you lock in the move

This is where downsizing becomes more than a property decision.

If you are eligible, the downsizer contribution can be a valuable way to move some sale proceeds into super. But it should not be treated as a simple bonus feature. It needs to sit inside your broader retirement plan.

Then there is the pension side. Once equity is turned into financial assets or super in pension phase, the assessment can change.

So the real question is not “Can I use the downsizer contribution?” It is “What does using it mean for my overall retirement position?”

Read more in Downsizer Super Contribution Explained and the government downsizer scheme page.

How iDownsize can help at this stage

This is where the Provider Network feature becomes useful again, particularly if you need to identify when it is time to speak with a financial adviser as part of your wider downsizing strategy.

Step 9: Avoid the most common downsizing mistakes

Most downsizing regrets are not caused by one dramatic blunder. They come from small errors in judgment that compound.

One common mistake is buying for emotion and selling for logic. People get emotionally attached to a shiny replacement property and then become overly transactional about the home they are leaving. Another is underestimating transaction costs. Another is assuming the next property only needs to suit current needs, not future ones. Another is staying too long in research mode until a health event, family change, or market shift forces rushed action.

There is also a quieter mistake: not making the move coherent.

A good downsizer move is not just “smaller.” It is cohesive. The location works. The property works. The finances work. The timing works. The support around it works.

That is the standard to aim for.

A practical timeline for downsizing in Sydney

Twelve to eighteen months out: clarify goals, explore possible suburbs, understand your likely equity position, think about what kind of property would actually work next.

Six to twelve months out: narrow options, test sell-first versus buy-first, identify what support may be needed, start reducing clutter and deferred maintenance.

Three to six months out: refine the move strategy, engage the right providers, prepare the home for market, sharpen the numbers.

Zero to three months out: execute the sale, secure the next property, manage the move logistics, and complete the financial follow-through.

Not every move takes that long, but treating it as a staged process almost always reduces pressure.

Where iDownsize fits into the whole journey

The strongest role for iDownsize is not as a single tool. It is as a connecting layer across the entire downsizing journey.

At the start, it helps turn vague intent into a more structured plan through tools like Pathways and the Downsize Calculator. In the middle, it helps with suburb research through Suburb Navigation, home selection through Property Comparison, and support access through the Provider Network. For users actively searching, it can also help them access off-market properties.

If you want to see how real downsizers have approached the journey, the Case Studies page is also worth exploring.

That is why it works best when used progressively. You do not need to arrive with everything figured out. Most people will not.

Final thoughts

The best downsizing decisions in Sydney are rarely the fastest ones. They are the clearest ones.

A good move is not measured only by how much smaller the next home is. It is measured by whether your next setup is simpler, more suitable, financially stronger, and better aligned to how you want to live.

That is the real opportunity.

If you are over 60 and thinking about downsizing in Sydney, the smartest first move is not necessarily to call an agent or start inspecting properties this weekend. It is to get clearer on your goals, your likely numbers, your risk tolerance, and the shape of the support you may need.

Do that well, and the rest of the journey gets a lot easier.

FAQs

Is downsizing in Sydney after 60 worth it?

For many homeowners, downsizing in Sydney after 60 can reduce maintenance, improve convenience, lower ongoing costs, and release capital. Whether it is worth it depends on the property, the replacement home, the suburb, transaction costs, and the broader retirement plan.

Do you pay stamp duty when downsizing in NSW?

In general, yes. Transfer duty usually applies when buying residential property in NSW, including when downsizing into another home.

Can downsizing affect the Age Pension?

Yes. Downsizing can affect the Age Pension depending on how sale proceeds are held or used after the move, including whether they become assessable financial assets.

Is it better to sell first or buy first?

That depends on whether you value certainty or convenience more. Selling first usually reduces financial risk, while buying first can reduce disruption but may require a stronger finance strategy.

[…] A useful starting point is the main pillar guide: How to Downsize in Sydney After 60. […]